(Source: Bankrate)

The Student Loan Debt Crisis

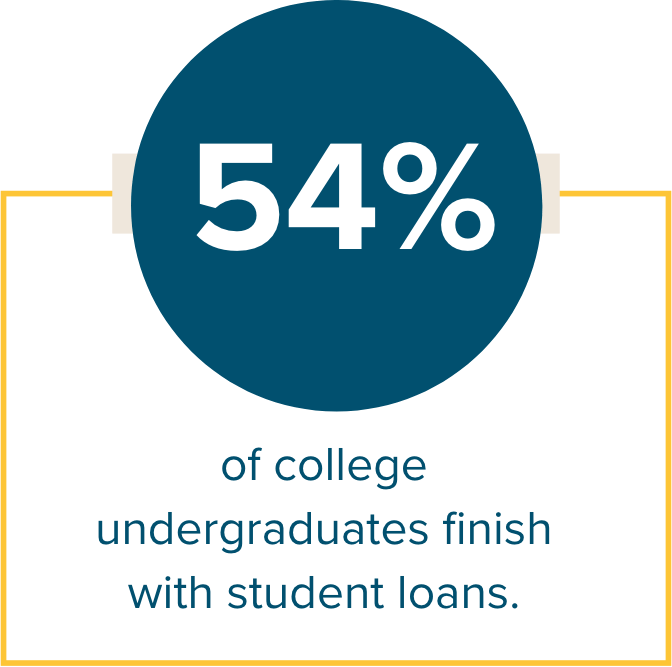

For many, student loan debt is a resource that provides the necessary financing for a college education. But it’s a double-edged sword: a resource and a liability. Without student loans, higher education would be inaccessible to many. But the student loan program is also complicated and confusing to borrowers.

The federal student loan program offers special benefits and borrower protections that aren’t available with other types of consumer loans. For example, multiple repayment options (some based on a borrower’s income), loan forgiveness and postponement options, and the ability to discharge loans in the event of disability or death.

Despite many attempts by loan servicers, schools, and third-party sources to help keep borrowers on track, some slip through the cracks. Default happens when a borrower has not made a payment for 270 days or more. Typically, the most vulnerable borrowers are disproportionately likely to default, as many of them have fewer resources to repay their loans. Due to the severe consequences of default — credit score damage, treasury offsets, wage garnishment, collection fees, etc. — borrowers with defaulted loans face barriers preventing financial health and security.

(Source: Education Data Initiative)

The Effects on the Multigenerational Workforce

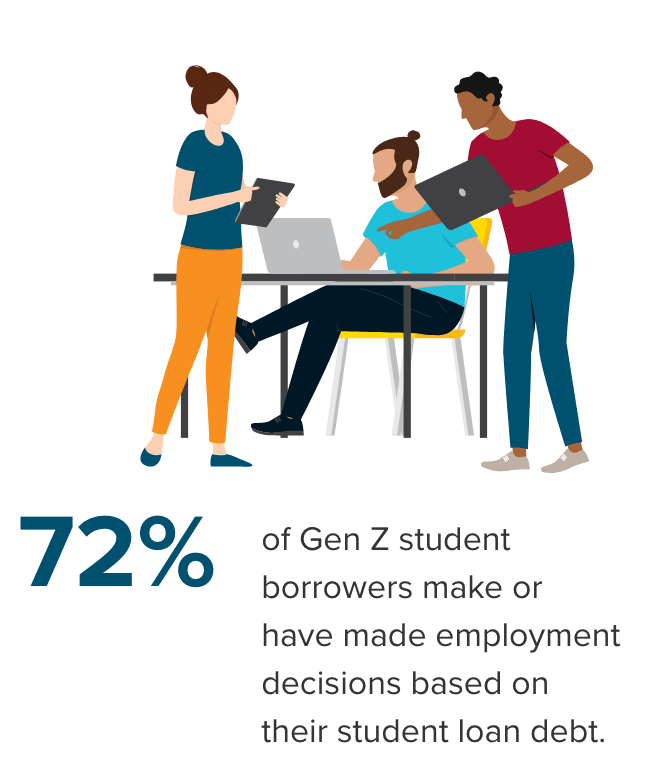

The effect student loan debt has on the economy has been likened to a recession. It reduces consumer spending, business growth, and homeownership and is likely to have economic consequences for U.S. businesses, communities, and citizens.

Student loan debt spans multiple generations and burdens each one differently.

| Generation Z |

|

| Millennials |

|

| Generation X |

|

| Baby Boomers |

|

Student Loan Debt Intersects with Well-Being

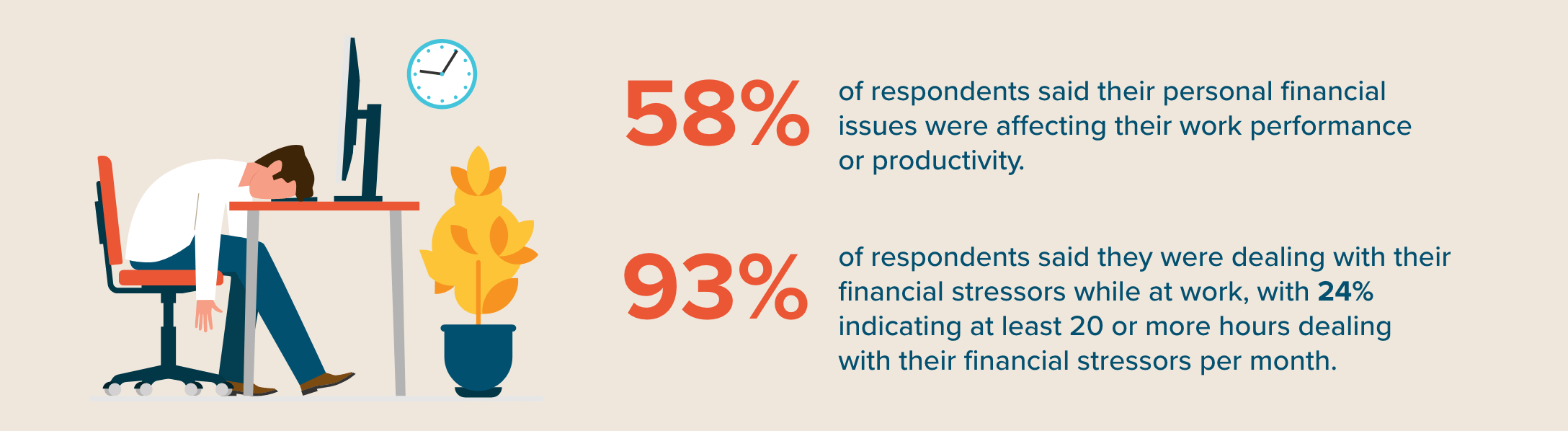

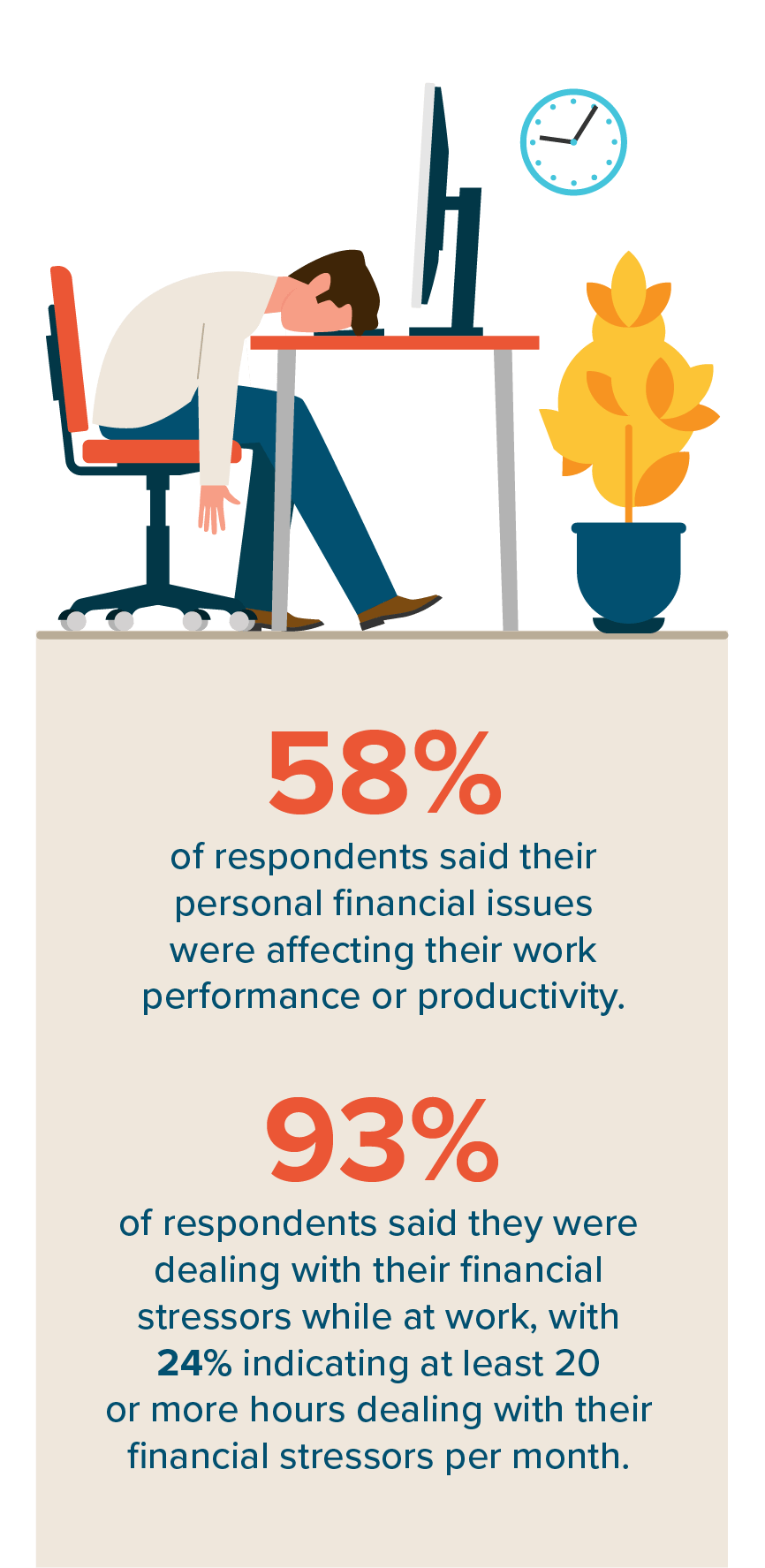

Over the past few years, the focus on well-being, particularly mental and emotional health, has increased. One of the most significant influences of this increased attention is the psychological impact of the trauma created by the COVID-19 health crisis. During this time, stress levels were elevated, and people were experiencing anxiety, depression, and loneliness. More people were compelled to acknowledge the trauma and address their symptoms.

The dimensions of well-being have become increasingly relevant as we begin to look at our health more holistically. The concept of well-being is subjective, and each of us may have a different view of what it means.

Well-being is multi-dimensional with varying influential factors such as financial, emotional, and occupational to name a few. The dimensions of well-being are interconnected. A problem or deficit in one area can impact others. For example, if a person has persistent stressors affecting their occupational well-being, it’s likely to impact their home life or social well-being. Likewise, improving an area can have a positive ripple effect. It’s also common to have greater health in one or more areas than others. Overall well-being doesn’t require all dimensions to be balanced.

“Last year, NASDAQ reported that 45% of workers consider student loan repayment assistance the single most important benefit, ranking it higher than additional retirement and health care contributions. ”

Student Loan Repayment Assistance

Student loan repayment assistance is an employee benefit that enables employers to make payments toward their employees’ student loans or make matching contributions to the employees’ retirement accounts when they make a student loan payment.

Employer Contribution (a.k.a. Student Loan Paydown):

A student loan repayment assistance employee benefit where an employer makes a contribution to employees’ student loans.

Employers can make tax-free payment contributions of any amount up to $5,250 per year, per employee. They can reimburse the employee like is done with tuition reimbursement, but most organizations make payments directly to the employee’s student loan lender or servicer. A $5,250 cap is the combined annual limit for education assistance payments — whether through tuition reimbursement or student loan repayment — and must be included as part of an Education Assistance Program.

Matching Retirement Contribution:

A student loan repayment assistance employee benefit where the employer makes a matching contribution to employees’ retirement accounts when employees make a student loan payment.

The SECURE 2.0 Act gives employers the option to make a matching contribution to the employee’s retirement plan, even if the employee is not actively, or fully, contributing to it. It permits an employer to make matching contributions under a 401(k) plan, 403(b) plan, or SIMPLE IRA with respect to qualified student loan payments.

SECURE 2.0 removes the dilemma that many workers face — they no longer must choose between saving for retirement or paying student loan debt.

Comprehensive Student Loan Support

In this highly competitive job market, Ascendium’s student loan repayment support is a great benefit to offer.

- Personalized 1:1 student loan counseling.

- Online financial education.

- A platform that allows employers to make contributions to employees’ student loans AND Make matching contributions to employees’ retirement accounts when they make a student loan payment.

The competition for top talent is fierce. A student loan paydown benefit helps you stand out.

Introducing this benefit is easier than you might think — our employer’s guide can help.

Student Loan Debt by the Numbers — for Employers

Use our interactive map to view student loan debt information by state.