Implementation of student debt letters was really picking up steam. From Washington to Florida and lots of places in between. The number of states with debt letter legislation (as of 2019) was up to 13. And then there was a pause that's lasted a year. Why?

Did discussions of an Federal Annual Student Loan Acknowledgement (ASLA) impact expansion? Perhaps, but keeping students informed is more important than ever. And introducing a personal message of support and campus resources to help student minimize indebtedness, as well as a plan for the future, is why the number of schools using debt letters continues to grow. Clearly this type of communication is more than a trend fueled by state mandates. With that in mind we’re republishing this 2019 post with 2020 updates.

Although there are differences in the state legislative requirements, there are also common threads like data, calculations, and proof of compliance. This blog post will summarize and drill it all down for you. But first, our legal team wants us to tell you it’s not meant to cover the intricacies of each state’s legislation and compliance requirements.

That being said, let’s take a look at the debt letter landscape.

|

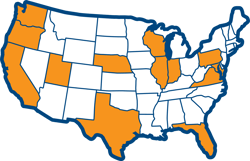

States Requiring Debt Letters

|

Who Wants What?

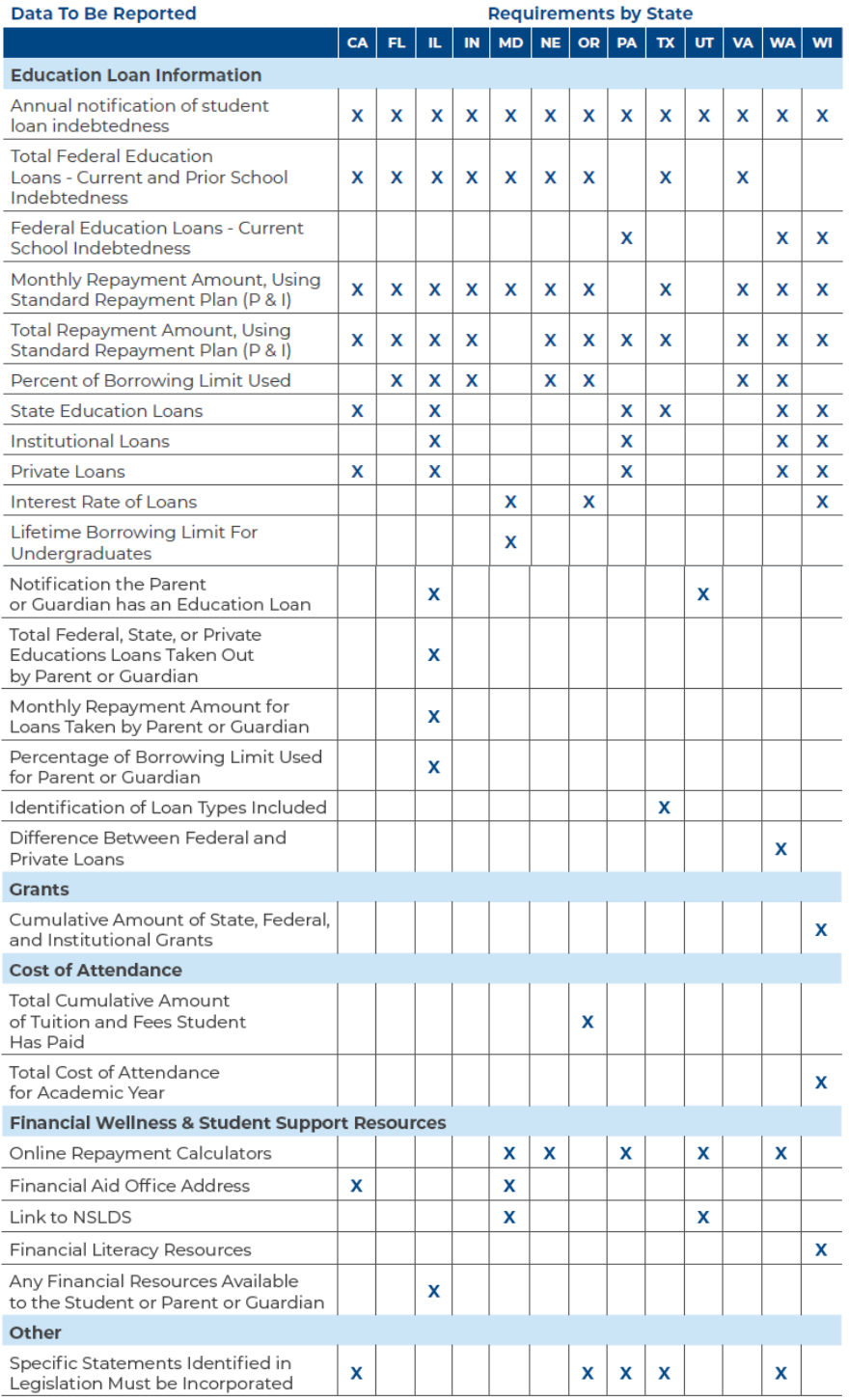

The commonalities and differences in state-based legislation for all 13 states are depicted in our Student Debt Letter Panorama table below, starting with the most popular data requirement—Federal education loans. Most states require federal indebtedness data from a borrower’s current and prior schools, loan totals and estimates for monthly payments and total repayment amounts. But some states also require the percent of borrowing limit a borrower has reached, ideally to help them plan for, or even limit, future borrowing.

Other requirements really depend on the individual state. For example, Illinois requires schools to not only present loan and percent of borrowing information for the student borrower, but also for the parent or guardian. Whereas Maryland requires schools to provide students with access to an online repayment calculator and a link to NSLDS.

Student Debt Letter Panorama

Download This Great Information In A Portable PDF.

Mining the Data

NSLDS is one of the main data sources where, depending on the state requirement, various loan details can be extrapolated. NSLDS data can provide details on federal loans, such as:

- Type of loan

- Loan balances from current and prior schools

- Interest rates

A school’s own data, pulled from their Financial Aid Management System, is also typically required. Together, the school data and what is found on NSLDS provide the base from which the communication can be created.

If your state doesn’t have debt letter legislation but you’re thinking about providing this type of information to your students, here’s a short summary of key data required by states with legislation.

- 100% require annual notification of student loan indebtedness.

- 85% require monthly and total repayment amount estimates using the Standard repayment plan.

- 54% feel percentage of borrowing limit used is critical to helping students manage their indebtedness.

- 46% require state, institutional or private loan data be provided to help round out the student’s borrowing picture.

- 39% have specific statements schools must include as part of the legislation.

How’s Your Math?

The tricky part of debt letters pertains to the math. Some of the calculations needed are relatively simple, like tallying up the total cost of attendance. However, others require complex algorithms to spin out accurate estimates that take into account different loan amounts, taken out at different time periods, and with different interest rates. Not to mention estimates related to the total projected amount of principal and interest, and estimated monthly payments.

Compliance Is Key

Given the legislative requirements in each state, proving you’ve done what you’re required to do is key. You can guess what we’re going to say next, right? Each state has different requirements on what to report and how to report it. Important considerations include what was sent (email or letter), when, to whom, and the frequency and method of reporting compliance. There’s also the auditing piece. In everything you do related to student loans, there’s the auditing piece, right? It can never be over-stated.

Questions?

Hopefully this 10,000 foot view of debt letter trends has been helpful. Have questions? Don’t hesitate to leave it below!